- Airlines serving large domestic markets are expected to see capacity bounce back to pre COVID-19 levels or even achieve growth.

- Recovery of carriers in Mainland China and the Asia-Pacific region is critical to the near-term delivery aspirations of aircraft manufacturers.

Signs of aviation recovery are emerging—especially in Mainland China and the Asia-Pacific Region, according to the global travel and data analytics expert Cirium. This is following the deepest drop seen in global air traffic since the start of the COVID-19 pandemic in April 2020.

Speaking on a Cirium-hosted webinar, Post Coronavirus Recovery for Aviation in China and the Asia-Pacific Region on June 23, 2020, Ascend by Cirium’s Head of Consultancy for Asia, Joanna Lu said, “The global market reached rock bottom in April 2020, and the only way now is up.”

“The air travel market in Mainland China is estimated to be down by 58% compared to the first four months of last year. However, while the international market has been hit hard since February, there are signs of recovery in the domestic market,” said Lu.

Some Asia-Pacific markets are bouncing back faster

The Asia-Pacific markets that are most reliant upon on international traffic and inbound tourism suffered the most. Hong Kong was the hardest hit, with April traffic down by over 73% compared with the same period in 2019. Taiwan (down 58.2%) follows Hong Kong and Singapore (down 48.4%) and Thailand (down 46.4%) at third and fourth.

Cirium’s global schedules data indicates a potential recovery across most Asia-Pacific markets through July 2020.

“Mainland China’s domestic schedule suggests a recovery to marginally positive year-on-year growth by end July, all and other regions are showing recovery as travel restrictions begin to ease. Those with large domestic markets are expected to see capacity back to pre COVID-19 levels or even growth by July,” said Lu.

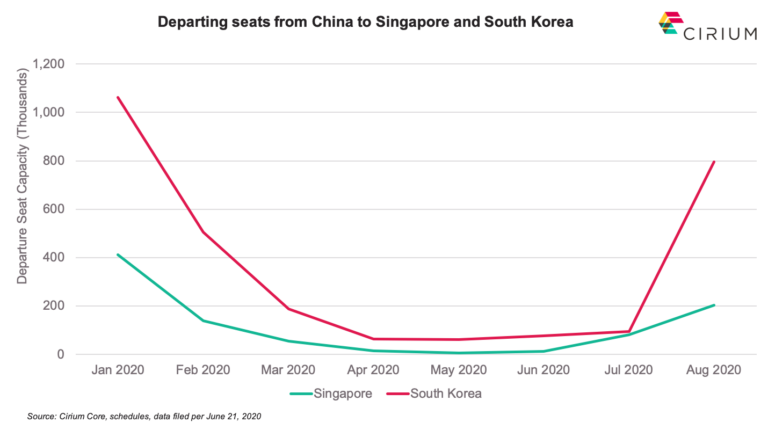

Unlike previous economically-driven downturns, post-COVID-19 intra-region recovery will likely be driven by bilateral agreements. For example, Mainland China is planning to establish “travel bubbles” with South Korea and Singapore for essential business travel. Other Asian COVID-19 bubbles now under discussion include Australia and New Zealand, Japan and Taiwan, Vietnam and Thailand.

Asia-Pacific airline recovery also key to aircraft manufacturer success

The recovery of airlines in Mainland China and the Asia-Pacific region is also critical to the near-term delivery aspirations of aircraft manufacturers (OEMs), according to Ascend by Cirium’s Global Head of Consultancy, Rob Morris who joined Lu on the webinar.

“Almost one-third of deliveries expected through 2023 are scheduled for the region. More than 1,360 deliveries are scheduled for Asia-Pacific operators, representing 31% of the total, compared to Europe at 29%, and North America at 22%,” said Morris.

The pace is picking up. The global parked aircraft fleet, which reached around 64% in mid-April 2020, is now below 50% as airlines return aircraft to service.

“We still expect to see several thousand aircraft remaining parked at the end of year. But the number will reduce as we see the recovery in Asia-Pacific, and also in North America and Europe, take shape.”

“Since March 1, 2020, almost 7,000 passenger jets have been returned to service by airlines globally, with more than 20% of them in Mainland China,” said Morris.

In regard to, the delivery projections of Airbus and Boeing, Morris noted that these are sensitive to a number of key assumptions. But, the most pessimistic global scenario is consistent with 3,500 single-aisle aircraft (1,980 from Airbus and 1,480 from Boeing), along with 900 twin-aisle aircraft (350 from Airbus and 550 from Boeing – delivered cumulatively through 2023. Current Market Values & Lease Rates are already starting to see negative pressure

Morris commented: “In a disrupted environment, it is very difficult to build a model that predicts future traffic growth with any precision. The demand outlook for 2020, 2021 and beyond is unclear because the dust hasn’t settled yet. However, a realistic recovery scenario suggests that the airline fleet in-service will remain below end 2019 levels until 2022 at the earliest.”

Source: www.cirium.com

#PacificAviationMarketing #PAM #GSA #airlines #travel #marketing #PR #HongKong #China